Deciphering Dark Pattern Litigation from an Economic Perspective

I. Introduction

“Dark patterns” is a term used to describe potentially deceptive app or website designs that could manipulate consumers to make choices they would otherwise not make. For example, by restricting or modifying how information is presented, these design features may lead consumers to pay fees or purchase subscription services they were not aware of or find themselves unable to cancel or pause services when they choose. In 2022, the Federal Trade Commission (“FTC”) released a report suggesting a rise in use of sophisticated dark patterns[1] and has since taken a more aggressive approach to prosecuting allegations of this conduct and regulating sellers.

Below are a few examples matters brought earlier this year:

- On January 4, 2024, the FTC and the Connecticut Attorney General took action against auto dealer Chase Nissan for allegedly violating Section 5 of the FTC Act and the Connecticut Unfair Trade Practices Act by charging “junk fees” and “unlawful add-on[s]” and by making misrepresentations about the price of certified used cars.[2]

- On June 17, 2024, the FTC alleged that Adobe violated the Section 5 of the FTC Act and the Restore Online Shoppers’ Confidence Act (“ROSCA”) by tricking customers into enrolling in subscription plans without proper disclosure of terms and by employing a complicated cancellation process to trap customers in subscriptions they no longer want.[3]

- On June 21, 2024, Connecticut resident Douglas Mundle brought a class action lawsuit against third-party bill payment company Doxo for allegedly violating the Washington Consumer Protection Act by using dark patterns to extract “unearned and unnecessary fees from consumers for the simple act of paying their bills online.”[4]

Several design choices now designated as “dark patterns” have been recognized as deceptive long before the terminology came into vogue. The recent designation of these designs as dark patterns reflects a current effort among academic, legal, and regulatory communities to distinguish between legal and illegal practices.[5] For example, the FTC amended its Negative Option Rule in October 2024, outlining specific seller behaviors that the FTC considers problematic, whereas prior to the amendment there were no regulatory standards regarding the simplicity of cancellation mechanisms.[6]

Economic analysis could prove useful in the ongoing attempts to define parameters around the legality of marketing design choices; however, there has been little discussion on the role of economic analysis in these cases. In this paper, we assess 46 dark patterns-related case filings from 2009 to 2024[7] and discuss the economic issues presented in these cases. In Section II, we provide an overview of the 46 dark patterns-related case filings. In Section III, we summarize the common allegations and key arguments in these filings. In Section IV, we discuss various methodologies for assessing liability and damages issues from the economic perspective.

II. Overview of Case Filings

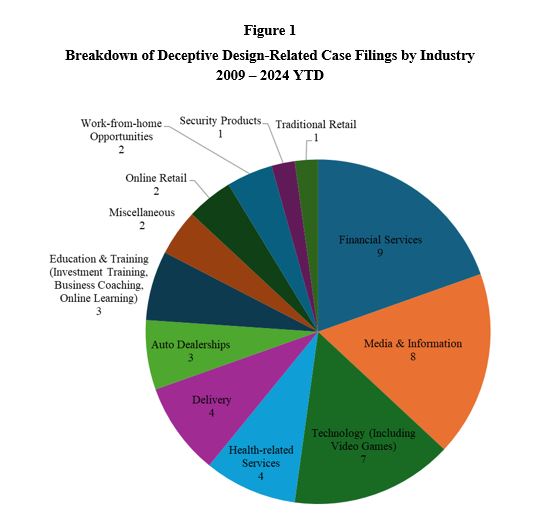

While the dark patterns-related allegations span many industries, our analysis shows that they are most prevalent in the service industry, including financial services, media and information, health, and delivery. Figure 1 shows the industry breakdown of the deceptive design-related case filings we examine in this paper.[8]

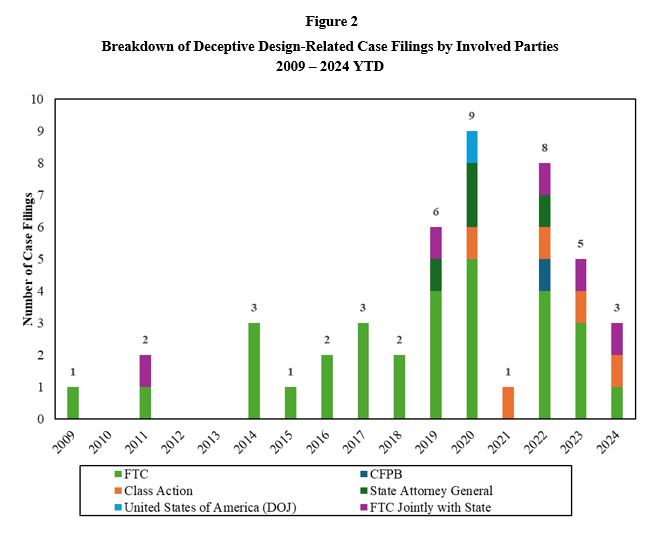

While the majority of these cases have been brought by the FTC, in recent years the FTC was joined by State Attorneys General and the Consumer Finance Protection Bureau (“CFPB”). Figure 2 shows an increase in case filings related to deceptive designs beginning in 2019. While one may plausibly attribute the increase to the growing use of the term “dark patterns,” the depicted cases were identified using additional search terms, including deceptive ad, free trial, cancellation, hidden costs/fees, automatic renewal, testimonial/endorsement, ranking, and negative option. The fact that we see a rise in cases even with the inclusion of these search terms may suggest an increased focus on deceptive designs generally that accompanied the rise in the use of the term “dark patterns.” As of 2020, at least one class action has been brought in each year.

III. Alleged Sources of Harm

In dark patterns-related cases, the allegations generally include three primary sources of harm to consumers: (1) failure to adequately disclose terms and conditions; (2) failure to provide a simple mechanism to cancel a subscription or membership; or (3) product misrepresentation. Examples involving the former include defendants allegedly failing to clearly disclose additional fees, subscriptions, or automatic renewal plans. Regarding cancellation mechanisms, defendants may allegedly hinder consumers’ ability to cancel subscriptions or obtain refunds. Examples of product misrepresentations include defendants allegedly making false product claims, using false celebrity endorsements, or displaying misleading independent or third-party reviews.

A. Failure to Disclose

The determination of what constitutes a materially misleading feature as opposed to a non-violative design choice requires careful assessment of the facts. Whether certain information was disclosed is often a straightforward question; whether it was disclosed in a way that consumers could appropriately understand is more ambiguous. Though required, the standard of “clear and conspicuous” sometimes leads to debate,[9] and courts have highlighted the importance of the impressions formed by consumers based on the information displayed.[10]

The difference in regulating “what to disclose” versus “how to disclose” is seen in cases related to the disclosure of subscription information. In Perkins v. The New York Times Company, a North Carolina customer sued The New York Times for violating the North Carolina Automatic Renewal Statutes and claimed that the company “fail[ed] to disclose clearly and conspicuously” automatic renewal offer terms and cancellation terms.[11] The Plaintiff claimed that “while the ‘Purchase Subscription’ button appears towards to bottom left of the webpage,” the disclosure of the subscription terms—specifically that the subscription will continue until the customer cancels it—is positioned near the top right of the webpage and appears indistinguishable from the surrounding block of unrelated disclosures.[12] In response to the Defendant’s motion to dismiss, the Court determined that the automatic renewal provision was sufficiently disclosed as the renewal terms were included in the checkout page. However, the Court sided with the Plaintiff regarding the claim that the Defendant’s cancellation terms were not conspicuously disclosed as they were “not highlighted and do not stand out from the dense, surrounding text,” and that therefore subscribers would need to “proactively search” for the cancellation policy.[13]

B. Failure to Provide a Simple Cancellation Mechanism

Prior to the recent amendments to the Negative Option Rule,[14] the FTC had no regulatory standard regarding the simplicity of cancellation mechanisms as compared to enrollment mechanisms.[15] On October 16, 2024, the FTC announced these amendments, which included the “Click-to-Cancel” rule, requiring sellers to design the mechanism to cancel a subscription or membership to be at least as simple as the mechanism the consumer used to enroll.[16] Even before the confirmation of the new rule, the FTC used the courtroom to argue in favor of simpler cancellation processes. For example, in FTC v. Vonage Holdings Corp. et al., the FTC claimed that the Defendants made the cancellation process difficult by requiring cancelling through a live agent during limited hours, obscuring contact information, requiring circuitous and redundant procedures, having long wait times, dropping and failing to answer calls, offering lengthy sales pitches, and charging expensive early termination fees.[17] By making cancellation difficult, the companies allegedly encouraged inaction (or failed action), thereby allowing them to capitalize on negative options.[18]

C. Product Misrepresentation

Businesses have also faced allegations that they misrepresented products or services by using false claims with respect to their products’ efficacy, thereby “tricking” consumers into signing up and paying for a product or service which they would otherwise not buy. In November 2023, the FTC brought a case against DNA testing company CRI Genetics, alleging that the company posted fake customer reviews on its own website and also allegedly posted high ratings on websites that were represented as third party sites but were actually owned by the Defendant itself.[19] In December 2023, the parties agreed to a settlement that prohibited the Defendant from misrepresenting any endorsement, rating, review, or connections it had with other websites or individuals—any endorsement needed to be from an actual user of the product and needed to be “truthful.”[20]

IV. Economic Analysis of Dark Patterns

A. Assessing Liability

Recognizing dark patterns and quantifying their impact is not a straightforward task. Some courts have relied on expert testimony to inspect the usability of websites and infer the impression consumers could get from the displayed information. For example, in 2009 the FTC sued Commerce Planet—a company that offered an internet auction kit through its platform OnlineSupplier—and claimed that the company tricked over 470,000 consumers into signing up for a monthly subscription when they thought they were merely signing up for a free kit. To support its claims, the FTC analyzed the landing and billing pages of OnlineSupplier to argue that the Defendants created the “net impression” that consumers are receiving a free kit when in reality consumers were left to pay monthly subscription fees. The Defendants allegedly made its negative option plan difficult for consumers to see on the sign-up pages.[21] The FTC’s expert applied a qualitative “usability inspection method” to analyze “what the user [could] perceive” by assessing if the webpage’s display of information was consistent with principles of usability.[22] The expert concluded that there was no basis to believe that “most people” would know about the monthly subscription or that the negative option existed upon visiting the webpages.[23] The Court found this expert testimony to be “on-point and persuasive.”[24] Furthermore, the Court criticized the Defendants’ strategy of minimizing the FTC’s expert’s testimony rather than producing their own expert report rebutting her arguments.[25]

The usability inspection is essentially a survey approach that tests for consumer understanding to assess whether consumers would be tricked by certain techniques—i.e., whether consumers are more likely to purchase the product when they are exposed to an alleged dark pattern design. However, identifying such a causal relationship requires valid and sound assumptions, and alternative approaches may be useful in providing more robust support to assess liability. For example, customer-level data (including order data, refund data, cancellation data, retention data, etc.) can be used to evaluate why consumers purchase the product or sign up for the subscription services and why they stopped using the product/service.

From an economic standpoint, consumers’ purchasing patterns derived from the data are also important to consider when assessing whether the consumers’ decisions to purchase are a result of exposure to the alleged dark pattern or merely an expression of the consumers’ interest in the product itself. For example, purchase histories can be assessed to better understand consumer behavior and infer preferences. If a company’s data show that the majority of customers re-subscribe or re-purchase the product after months with paused subscription or no purchase, then a reasonable consumer’s purchases or participation in the subscription plan may reflect their genuine demand. On the other hand, if nearly all products were returned, then perhaps the consumer found the product to be non-viable. With this in mind, an economist might infer that consumers’ purchasing decisions were likely influenced by the dark patterns—the consumers would not have purchased the product had they not encountered the dark pattern.

B. Assessing Damages

In many of the dark patterns-related cases, plaintiffs’ request for monetary equitable relief can take the form of restitution or disgorgement. Restitution may be measured by the “the full amount lost by consumers,”[26] where net consumer loss is usually calculated by “the amount of money paid by the consumers, less any refunds made” and any value received by the consumers.[27] In contrast, disgorgement is measured by the profits causally connected to the alleged violation. Most of the recent cases resulted in permanent injunction and restitution.[28]

Calculating consumer loss involves aggregating the sales made to consumers harmed by the alleged conduct, adjusting for company refunds or returns. In these cases, to quantify damages, it is necessary to appropriately identify the population of consumers purportedly harmed by the alleged conduct. In calculating damages, experts introduce a number of assumptions. For example, in FTC v. Commerce Planet, Inc. et al., the FTC’s expert’s calculation of consumer loss relied on two assumptions: (1) no consumer would have joined OnlineSupplier if the nature of the membership had been fully disclosed to them, and (2) consumers derived no benefit from their OnlineSupplier memberships.[29] Therefore, any consumer who signed up as OnlineSupplier members during the relevant period would be included in the calculation of total consumer loss and the full amount paid by consumers, adjusting for refunds and returns, is equal to consumer loss.[30]

In response, the expert for Commerce Planet testified that the assumptions used in the plaintiffs’ damages analysis were unsupported, as a certain percentage of consumers cancelled within the trial period and consumers derived some value from the product, suggesting that the FTC’s total consumer loss was overstated as it included consumers who were not “harmed” or derived some value from the product (therefore not all payments from these consumers should be considered as consumer loss).[31] However, in its decision on calculating consumer loss, the Court stated that the FTC “need not show that all consumers were deceived, relied upon the misrepresentations, or that consumers did not derive any utility from the product.”[32]

In FTC v. Willms et al., the FTC’s estimated consumer injury was “predicated on the view that all of Defendants’ sales that were not returned to customers through company refunds or charge reversals by banks or credit card companies represent consumer injury.”[33] The Defendants questioned whether the FTC appropriately proved this presumption holds.[34] Further, the Defendants’ expert argued that “[i]n order to impute a magnitude to the alleged consumer injury it is necessary to compute a complaint rate” but that “[a] complaint rate alone could understate the incidence of consumer injury because some consumers might cancel a subscription without complaining and it could overstate the incidence because some people will complain even if they were aware of the terms and conditions, or they may complain in multiple venues.”[35] Ultimately, the Court ruled in favor of the FTC, finding the Defendants liable for using deceptive designs and making unauthorized charges to consumers’ credit cards.[36]

Assumptions made in assessing damages could be supported by the company’s data. If the data show that a substantial portion of purchases were made as a result of genuine demand, then it may be unreasonable to assume all purchases were due to the company’s purported deliberate misguidance and that these purchases should be attributed to consumer loss. Moreover, consumers may suffer harm to varying degrees given that different subsets of consumers may be differently situated. A consumer who enrolled in a company’s subscription plan but otherwise has no sales activity with the company may have a different loss compared to a consumer who enrolled and made purchases frequently. One should recognize the different types of consumers when distinguishing the different levels of consumer loss.

V. Conclusion

Economics plays an important role in assessing issues of liability and damages in dark pattern-related litigation because so far, the use of “dark patterns” has not been defined as a violative practice. Instead, as we have shown above, designs that are now being identified as dark patterns have long been enforced against to the extent that their use falls under existing authorities for unfair or deceptive acts and practices. As such, experts can perform analyses to assess the usability of websites and infer the impression consumers get from the display of information to determine if design features deceive consumers. Experts can also analyze customer-level data on purchasing patterns, refunds, and cancellations to determine whether consumers’ decisions were influenced by dark patterns or reflected genuine demand, and further, to identify potentially harmed consumers and consumer loss. Overall, rigorous economic analysis is essential for objectively evaluating the merits of dark pattern-related allegations and ensuring fair outcomes in these cases.

CITATIONS

[1] FTC Staff, “Bringing Dark Patterns to Light,” September 2022 (“Bringing Dark Patterns to Light”), https://www.ftc.gov/system/files/ftc_gov/pdf/P214800%20Dark%20Patterns%20Report%209.14.2022%20-%20FINAL.pdf.

[2] Complaint for Permanent Injunction, Monetary Judgment, Civil Penalty Judgment, and Other Relief, FTC and State of Connecticut v. Chase Nissan, LLC, et al., United States District Court for the District of Connecticut, Case No. 3:24-cv-00012, January 4, 2024.

[3] Complaint for Permanent Injunction, Monetary Judgment, Civil Penalty Judgment, and Other Relief, U.S. v. Adobe, Inc. et al., United States District Court for the Northern District of California, Case No. 5:24-cv-03630-BLF, June 17, 2024.

[4] Class Action Complaint, Douglas Mundle v. Doxo, Inc. et al., United States District Court for the Western District of Washington, Case No. 2:24-cv-00893, June 21, 2024.

[5] Shaheen, R. and Mudge, A., (December 2021). “Dark Patterns or Savvy Marketing—Where is the FTC’s Focus on Dark Patterns Taking Us?” Antitrust Magazine Online, p. 2. See Figure 2.

[6] “Negative Options” refers to terms and conditions which allow a company to interpret a consumer’s silence or inaction as acceptance. The amendments prohibit sellers from (1) misrepresenting material facts with a negative option feature; (2) failing to clearly and conspicuously disclose terms prior to obtaining billing information in connection with a negative option feature; (3) failing to obtain express informed consent before charging a consumer; and (4) failing to provide a simple mechanism to cancel a subscription or membership.

[7] We compiled these cases using LexMachina and the website Deceptive.Design based on the following search terms: dark pattern, deceptive ad, free trial, cancellation, hidden costs/fees, automatic renewal, testimonial/endorsement, ranking, and negative option. While we recognize that this list may not be exhaustive, we believe that it still provides a helpful overview of the dark pattern case landscape.

[8] We reviewed descriptions in each case filing to determine the industry in which the allegation takes/took place.

[9] See 15 U.S.C. §§ 41-58. See also 15 U.S.C. §§ 8401-8405.

[10] For example, in CFPB v. TransUnion et al., some of the specific design features alleged to be deceptive by the CFPB included: (1) those that gave consumers the impression they could directly “get” or “see” a standalone credit score after clicking a button, when instead the button led to a subscription enrollment page and (2) those that gave consumers the impression that their credit card information would be used for identification purposes only, when in fact the card was stored for use in the subscription enrollment. See Complaint, CFPB v. TransUnion et al., United States District Court for the Northern District of Illinois Eastern Division, Case No. 1:22-cv-01880, April 12, 2022, ¶¶ 38 and 40.

[11] Class Action Complaint and Demand for Jury Trial, Megan Perkins v. The New York Times Company, United States District Court for the Southern District of New York, Civil Action No. 1:22-cv-05202, June 21, 2022 (“Perkins Complaint”).

[12] Perkins Complaint, ¶ 25.

[13] Opinion and Order, Megan Perkins v. The New York Times Company, United States District Court for the Southern District of New York, Civil Action No. 1:22-cv-05202 (PKC), May 23, 2023, pp. 6–9.

[14] See supra section I.

[15] The FTC built upon ROSCA, expanding rules around internet sales to other markets including telephone, internet, traditional print media, and in-person transactions. See Federal Register, Proposed Rules, April 24, 2023, Vol. 88, No. 78, section II, https://www.federalregister.gov/documents/2023/04/24/2023-07035/negative-option-rule.

[16] “Click-to-Cancel” Rule Announcement.

[17] Complaint for Permanent Injunction, Monetary Relief, and Other Relief, FTC v. Vonage Holdings Corp. et al., United States District Court for the District of New Jersey, Case No. 3:22-cv-6435, November 3, 2022, ¶ 3.

[18] See Bringing Dark Patterns to Light, footnote 83. See also CFPB Circular 2023-01, p. 1.

[19] Complaint for Permanent Injunction, Civil Penalties, and Other Relief, FTC and the People of the State of California v. CRI Genetics, LLC, United States District Court for the Central District of California, Case No. 2:23-CV-9824, November 20, 2023.

[20] Stipulated Order for Permanent Injunction, Monetary Judgement for Civil Penalty, and Other Relief, FTC and the People of the State of California v. CRI Genetics, LLC, United States District Court for the Central District of California, Case No. 2:23-CV-9824-RGK-AGR, December 11, 2023, p. 8.

[21] Complaint for Permanent Injunction and Other Equitable Relief, FTC v. Commerce Planet, Inc. et al., United States District Court for the Central District of California, Case No. SACV-09-01324 CJC (RNBx), November 10, 2009, ¶¶ 14–19.

[22] Principles of usability include “the fact that users typically do not scroll, tend to scan very quickly and read only 20% of what is on the page”. See Memorandum of Decision, FTC v. Commerce Planet, Inc. et al., United States District Court for Central District of California Southern Division, Case No. 8:09-cv-01324 -CJC (RNBx), June 22, 2012 (“Commerce Planet Decision”), p. 26.

[23] Commerce Planet Decision, p. 26.

[24] Commerce Planet Decision, p. 25. Importantly, the Court noted that Section 5 of the FTC Act requires that perceptions are measured “from the perspective of a reasonable consumer, not that of the seller or the seller’s employee.” See Commerce Planet Decision, p. 28.

[25] Commerce Planet Decision, p. 31. The Defendants offered an analysis of user data, arguing that most consumers understood the negative option plan when they signed up for OnlineSupplier. The Court sided with the FTC’s consumer injury expert that the Defendants’ user data-based argument was “uncorroborated by the evidence in the record.” (Commerce Planet Decision, pp. 31–32).

[26] Commerce Planet Decision, p. 60.

[27] Commerce Planet Decision, p. 60. Quantifying this amount requires an assumption about value received by consumers. Non-monetary costs might also be included in the calculation. This requires a valuation of a consumer’s time or other “costs” incurred during an encounter with a dark pattern design.

[28] Of the 46 cases we relied on, 5 have been dismissed and 3 remain unresolved. Of the other 38 cases that were resolved, at least 20 have resulted in restitution, and 35 have resulted in some sort of monetary relief.

[29] Commerce Planet Decision, p. 62.

[30] Commerce Planet Decision, p. 62. The FTC’s expert assumed that consumers did not value Commerce Planet’s product, and that therefore no such value should be subtracted from consumer loss.

[31] Commerce Planet Decision, p. 64.

[32] Commerce Planet Decision, p. 64. In its decision on liability, the Court decided that the Defendants’ focus “on a few satisfied customers and the utility of the product being sold” was incorrect. Rather, the focus should be on an analysis of “misrepresentations made about the product.” The Court was not satisfied by the fact that “a few” customers of OnlineSupplier found it to have some utility. See Commerce Planet Decision, p. 33.

[33] Declaration of Richard S. Higgins, FTC v. Jesse Willms, et al., United States District Court for the Western District of Washington at Seattle, Case No. C11-00828-MJP, July 18, 2011 (“Higgins Declaration”), ¶ 5.

[34] Higgins Declaration, ¶¶ 6–7.

[35] Higgins Declaration, ¶¶ 16–17.

[36] See Stipulated Final Judgment and Order for Permanent Injunction and Monetary Relief as to Jesse Willms; 1021018 Alberta LTD; 1016363 Alberta LTD; 1524948 Alberta LTD; Circle Media Bids Limits; Coastwest Holdings Limited; Farend Services LTD; JDW Media, LLC; Net Soft Media, LLC; Sphere Media, LLC; True Net, LLC; and Mobile Web Media, LLC, FTC v. Jesse Willms, et al., United States District Court for the Western District of Washington at Seattle, Cas No. 2:11-cv-828-MJP, March 6, 2012.

Experts

Partner

Partner Principal Consultant

Principal Consultant Juliet Bellin WarrenSenior Consultant

Juliet Bellin WarrenSenior Consultant